The Wrong ROI Question for AI

Evaluating AI with throughput accounting vs cost accounting principles

Efficiency is an easy question to ask about. It is easy to measure. It probably matters in some parts of a company. If a team can produce the same report in twenty minutes instead of four hours, or answer the same support question without a human stepping in, there is real value there.

But that question is also too small.

Accounting Models Become Culture

A while back I got interested in throughput accounting. I’m not an expert. I haven’t taken courses on it, and I haven’t watched it operate inside a company firsthand. But it’s an idea I’m curious about, and I see more and more applications for it in the world of AI.

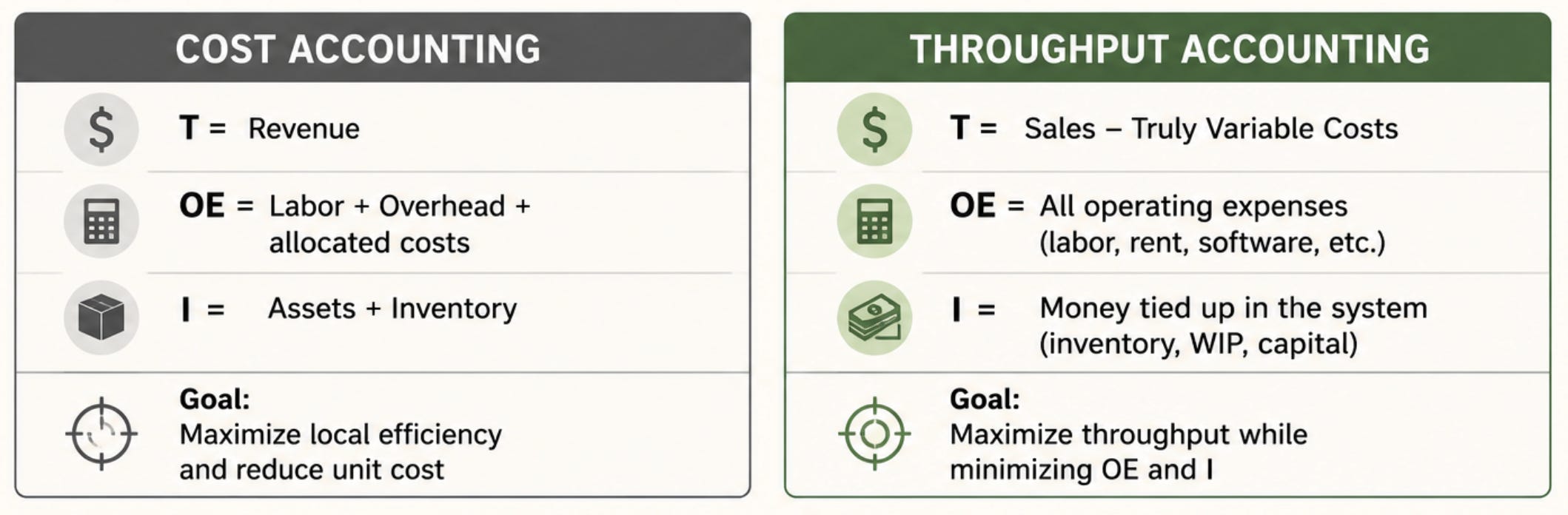

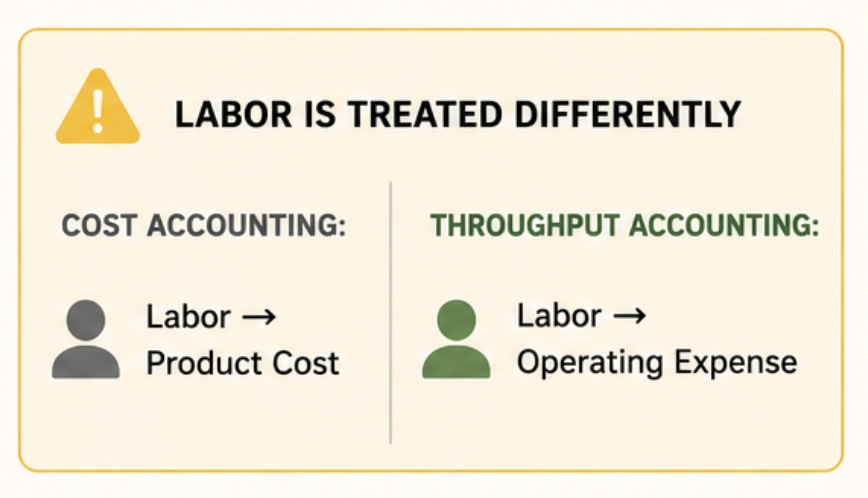

The way I understand it, throughput accounting is partly a foil to traditional cost accounting. Cost accounting teaches a company to see financial health through costs, utilization, efficiency, and expense control. Throughput accounting starts from a different assumption: the goal is not to keep every resource busy, but to increase the flow of value through the system.

This will be a problem for companies adopting AI because accounting models become company culture. A company that manages through cost accounting starts to protect utilization. So AI will be asked to justify itself, and the first version of the ROI question will probably be: How much time did it save? How many tasks did it automate? How many people can now do the work of more people?

Why Lean Gets Misread

One reason Lean can be so hard to practice inside a large company: it gets talked about as an efficiency system, but that framing misses much of what makes it work.

Lean needs slack, flow, learning, small experiments, and the ability to see and respond to constraints in the system. It asks teams to reduce certain kinds of waste, but not by keeping every person maximally busy every minute. That ask can feel almost backwards to a company trained to worship utilization.

If every person needs to be fully allocated, who has room to improve the system?

If every team is measured by whether they hit the original plan, who has permission to learn that the plan was wrong?

If every budget conversation turns into a defense of headcount and expense, who is rewarded for creating options that may not pay off this quarter?

There is value in that. Some work should get cheaper. Some repetitive work should go away. Some workflows really are just slow versions of things machines can now help with.

But if that is the main frame, AI gets pulled into the same worldview that made Lean difficult to adopt. It becomes another way to squeeze more output from the existing system instead of a way to question or expand the system itself.

The more interesting possibility is that AI lowers the cost of exploration. A team can compare ten ways to frame a customer problem before picking one or explore more interaction patterns before committing to a prototype. Engineers can pressure-test an approach or understand unfamiliar code faster.

None of that is automatically valuable. AI can also create noise, false confidence, shallow work, and a flood of plausible nonsense. Exploration still needs taste, judgment, contact with reality, and some disciplined way to decide what evidence matters. But the cost curve changes.

When exploration is expensive, companies naturally ration it. They ask for a business case before the learning has happened. They ask teams to prove the opportunity before giving them time to understand it. They ask for confidence at the exact moment when confidence should still be low.

AI does not remove that problem, but it changes the excuse. If the cost of trying more paths goes down, the bottleneck is no longer just capacity. It’s whether the company is willing to treat learning as legitimate work. That’s a budgeting question as much as a technology question, and this is where I see throughput accounting as a valid idea to explore.

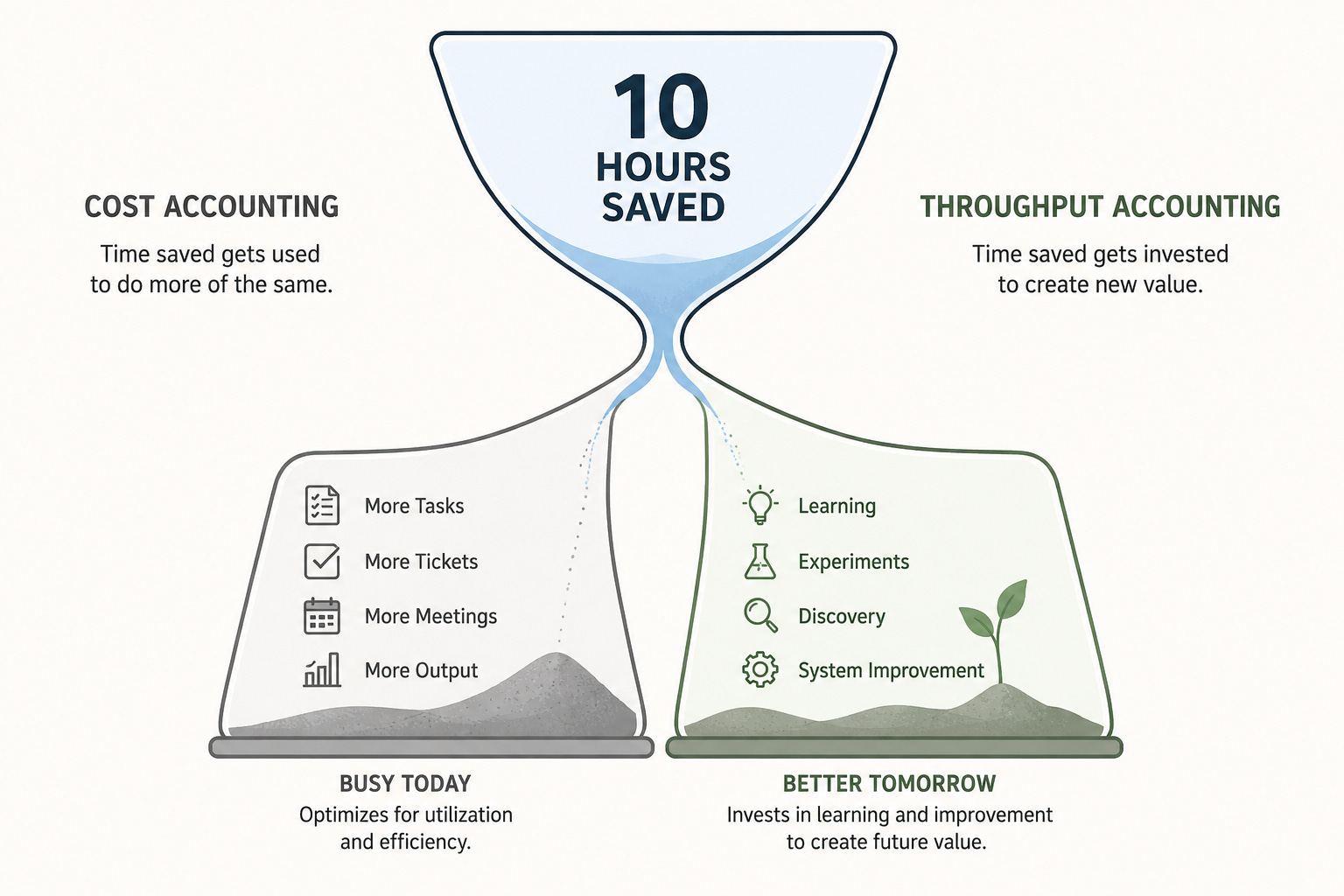

Saved Time Is Only Valuable If You Spend It on Better Bets

Imagine a team that adopts AI and saves ten hours a week. A cost-accounting worldview immediately asks how to fill those ten hours. Can the team take on more tickets? Can the headcount plan shrink? Can the same people support more projects?

A throughput-oriented worldview asks a different question: what value does those ten hours create?

Could the team test a riskier assumption? Could they explore where to improve the system that keeps creating rework? Could they propose a new revenue path that previously felt too speculative to touch?

Two Different Theories of ROI

The difference is more than preference for creativity over discipline, it’s an entirely different theory of where money comes from. If you believe the company’s main problem is that labor is too expensive, then AI should make labor cheaper. If you believe the company’s main problem is that it is too slow to discover and exploit valuable opportunities, then AI should increase learning throughput.

Those two beliefs lead to very different behavior.

The cost accounting belief turns AI into an extraction tool. It asks people to do the same work faster, then fills the freed space with more of the same work.

The through accounting belief turns AI into an option-creation tool. It asks what the company can now afford to learn, test, or attempt that used to be too slow or too costly.

The Lean Trap, Repeated

This is where the Lean comparison matters. A lot of companies wanted Lean results without changing the management assumptions that made Lean possible. They wanted speed without slack, learning without variation, quality without stopping the line, and continuous improvement without giving teams time to improve anything.

AI could suffer the same fate.

Companies may want AI outcomes without changing the budgeting logic around the work. They may want innovation while measuring everyone by utilization. They may want experimentation while punishing the appearance of unused capacity. They may want new growth while treating every saved hour as a cost-reduction opportunity.

The danger is not that AI will fail. The danger is that it will work just well enough to reinforce the wrong habit.

A company might become faster at producing documents nobody needs. Faster at building features that do not matter. Faster at analyzing markets it will not enter. Faster at generating plans that still avoid the hardest uncertainty. The dashboard will show productivity gains, but the business may not become more adaptive.

That is the second-order problem. Once AI makes output cheaper, output becomes a worse signal. More drafts, more tickets, more research summaries, more prototypes, and more strategy documents may say less than they used to. The scarce thing becomes the ability to choose, learn, and change direction based on what is learned.

The Real Divide

So the practical test is simple: when AI saves time, where does the time go? If it only disappears into more productivity metrics, the company is probably using AI as a cost tool. If some of that time gets deliberately reinvested into customer learning, product discovery, system improvement, technical quality, or new revenue exploration, then AI has a chance to become something more strategic.

This does not mean every AI gain should become exploration. Companies still need discipline. They still need operating leverage. They still need to stop funding vague experiments that never meet reality. Throughput is not an excuse for wandering.

But if every AI conversation has to justify itself through cost reduction, the company may never see the larger opportunity. It will ask the tool to make the existing machine cheaper instead of asking whether the machine is pointed at the right opportunity.

That is the part I keep coming back to. AI may not tell us which companies are technologically advanced. It may tell us which companies have a management system capable of learning. The ones that treat saved time only as saved cost will get efficiency. The ones that can turn saved time into better exploration may find something more valuable.